CPC (TDS) Advisory for Tax Credits in 26AS with respect to Tax Deducted on Sale of Immovable Property (26QB Statement)

As per section 194IA of the Income Tax Act, buyer is required to deduct tax at source @1% of the amount paid/credited to the seller. Therefore, after processing of 26QB statements, the information will appear in 26AS of buyer & Seller in the following manner:-

Scenario 1

If Buyer has deducted & deposited Rs.50,000/- on payment of Rs.50,00,000/-.

Seller:

TDS Credit is reflected in Part A2 of the seller to the extent of 1% of amount paid/credited. This credit is available for claim in ITR by the seller .

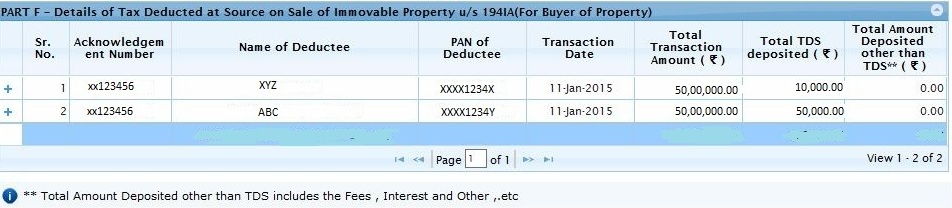

Buyer:

Total tax deposited by buyer is shown in Part F of 26AS of Buyer for information. Part F information is not available for Claim in ITR of buyer.

Scenario 2:

If Buyer has deducted & deposited Rs.60,000/- on payment of Rs.50,00,000/-.

Seller:

TDS Credit is reflected in Part A2 of the seller to the extent of 1% of amount paid/credited. This credit is available for claim in ITR by the seller.

Buyer: (i) Excess Tax Deposited by buyer i.e. Rs.10,000.00(Rs.60000-Rs.50000) is shown in Part A2 of 26AS of Buyer. This credit is available for claim in ITR of Buyer.

Buyer: (ii)

Total tax deposited by buyer is shown in Part F of 26AS of Buyer for information. Part F information is not available for Claim in ITR of buyer.

CPC (TDS) TEAM